Engine Failure Insurance: What Your Warranty Actually Covers

"Your engine just failed. Does your warranty cover it? Spoiler: most policies exclude 'pre-existing conditions' and 'modified vehicles.' Here's what actually gets covered, and what doesn't."

Engine

8/10

Gearbox

8/10

Electric

7/10

Total Risk

3/10

Quick Verdict

BuyA highly reliable luxury option. Buy with confidence but verify service history.

Reliability Verdict

Excellent long-term reliability profile with manageable routine maintenance costs. Powertrain is solid, but electronics require periodic updates.

Executive Intelligence Summary

Can you insure your engine against failure? Understanding Mechanical Breakdown Insurance (MBI) vs. traditional auto insurance for luxury car owners.

In This Guide

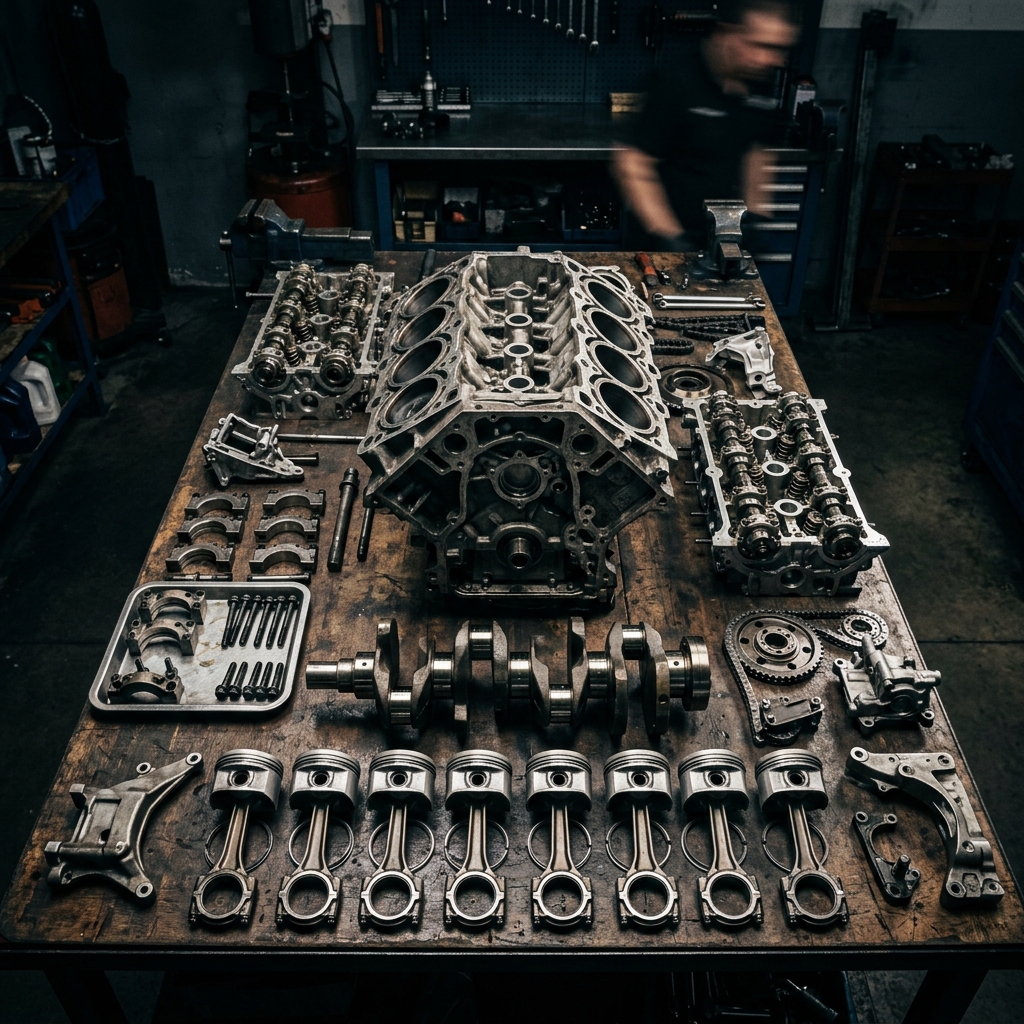

Many high-end car owners believe their standard full-coverage insurance policy will help if their engine explodes. This is a dangerous misconception. Traditional auto insurance only covers damage from external events (accidents, fire, theft, falling objects). If your BMW S55 crank hub slips or your Range Rover timing chain jumps, standard insurance will pay $0.

However, there is a specialized product often overlooked by luxury buyers: Mechanical Breakdown Insurance (MBI).

What is Mechanical Breakdown Insurance (MBI)?

MBI is insurance that functions like an extended warranty but is regulated as an insurance product and typically purchased through your auto insurance provider (e.g., GEICO, Allstate).

MBI vs. Extended Warranty

- Cost Structure: MBI is usually a small monthly addition to your premium (e.g., $10-$30/month) rather than a $5,000 upfront lump sum.

- Regulation: MBI is highly regulated by state insurance commissioners, meaning the “fine print” is often more consumer-friendly than some third-party warranty contracts.

- Eligibility: You must typically add MBI when the car is almost new (e.g., under 15,000 miles and less than 15 months old). It then stays active for up to 7 years or 100,000 miles.

Does MBI Cover Catastrophic Engine Failure?

Yes. If your engine suffers a mechanical failure that is not caused by lack of maintenance (e.g., you never changed the oil) or modification (e.g., you tuned the ECU), MBI will cover the replacement.

The Luxury Car Catch: Most MBI policies have a payout limit based on the vehicle’s Actual Cash Value. This is critical for cars like Ferraris or older AMGs. If an engine replacement costs $50,000 but the MBI policy has a lower cap for exotic internals, you could be left with a massive bill.

Key Coverage Areas for Luxury Owners

- Internal Engine Components: Pistons, cams, valves, and crankshafts.

- Turbochargers & Superchargers: Often the first items to fail in high-strung luxury engines.

- Control Modules: The “brains” of the car that can cost $3,000+ each.

- All-Wheel-Drive Systems: Differential failures and transfer case issues.

Common Reasons for Claim Denial

- Modifications: If you have an aftermarket intake, exhaust, or ECU tune, your engine failure claim will likely be denied.

- Overheating: If you continue to drive the car after it warns you of low coolant, the resulting engine damage is considered “owner negligence” and is not covered.

- Maintenance Gaps: You must prove with receipts that you followed the manufacturer’s oil change and inspection intervals exactly.

Verdict

If you are buying a used luxury car with high mileage, MBI is likely not available to you; you must look at Extended Warranties.

If you are buying a new or delivery-mileage luxury car, adding MBI to your insurance policy is a “no-brainer.” It provides the same protection as an extended warranty for a fraction of the upfront cost.